Something happens in the back half of 2026 that has never happened before. Three of the most valuable private companies on earth are planning to go public inside the same capital window.

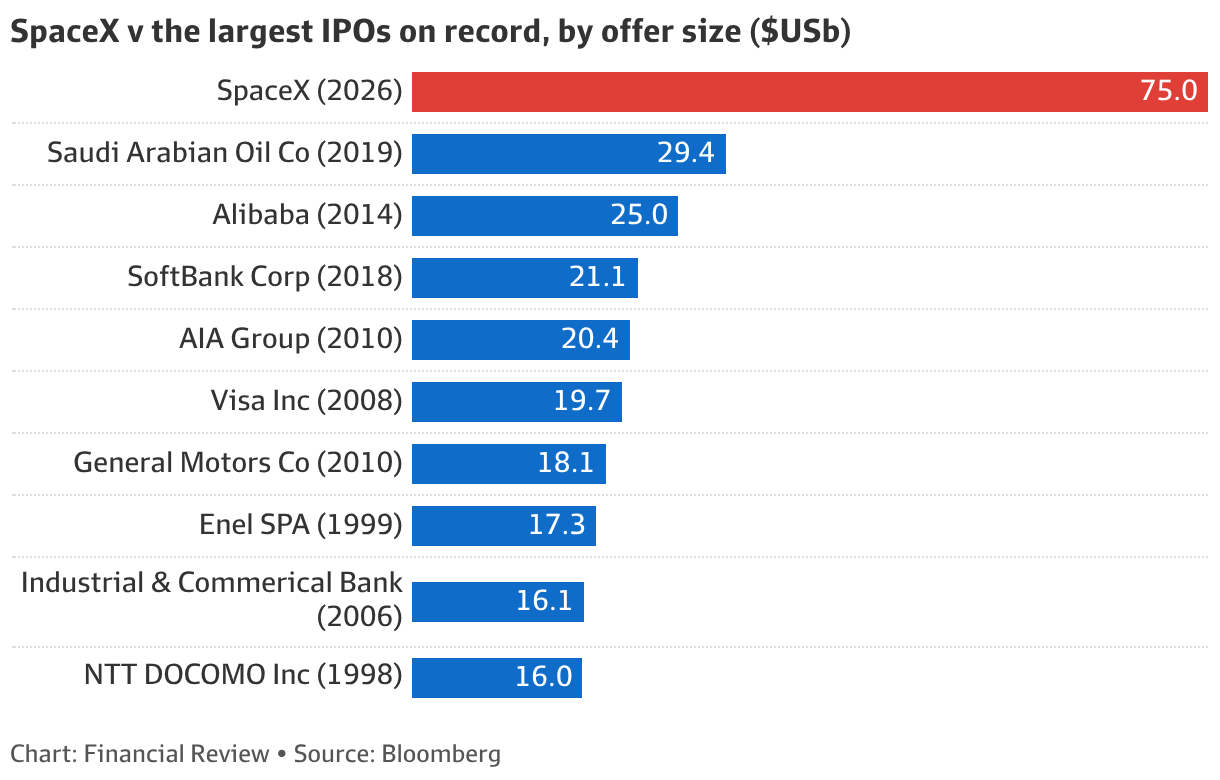

SpaceX filed first. Its prospectus is targeting a valuation north of 1.75 trillion dollars and a raise around $75 billion - which would make it the largest IPO in history, more than doubling Saudi Aramco’s record. OpenAI filed confidentially behind it, targeting somewhere between $850 billion and over a trillion. Then Anthropic filed days after closing a round that valued it at $965 billion, leapfrogging OpenAI on the way past.

Add it up and you’re looking at the better part of four trillion dollars in market value trying to list at roughly the same time.

That money has to come from somewhere. And here’s the part that should make you sit up: some of it is already yours.

.jpeg)

The bit nobody’s putting on the front page

You’re not going to get a phone call asking if you’d like to fund Elon Musk’s Mars factory. You don’t need to. If you’ve got super - and you do - a chunk of it sits in indexed global equity funds. The moment these companies enter the major indices, every passive fund tracking those indices is forced to buy. Not because a fund manager looked at the numbers and liked them. Because the rules of index-tracking say you hold what’s in the index, at the weight it’s in the index, full stop.

It’s the blessing and a curse of holding part of an index fund and there are ‘stop-gaps’ to protect the integrity of the index. Sorry, there were stop-gaps designed to protect the integrity of the index. More on this later.

Fortune put it bluntly this month: the S&P 500 will initially exclude SpaceX, but Musk is “coming for your retirement savings anyway.” The mechanism is forced buying. A mega-IPO with a small free float can create a demand spike the moment it qualifies for inclusion, and the buyers aren’t choosing - they’re complying.

So before we even get to whether these are good businesses, sit with that. You are likely about to be a shareholder in all three. You will not have been asked. And in at least one case, even if you owned the shares directly, you’d have almost no say in how the company is run.

SpaceX: the clusterf*#k of messy ideas for any retail investor

Let’s start with the numbers, because they’re public now and they tell a story the headline valuation doesn’t.

SpaceX did $18.67 billion dollars in revenue in 2025. Rightio! It lost $2.59 billion at the operating line and posted a net loss near $4.9 billion. The year before the picture was different - it actually made a $791 million dollar profit in 2024.

What changed? In February, SpaceX absorbed Musk’s AI company, xAI - which already owned X, the platform formerly called Twitter, and the Grok model. So one filing now contains four businesses under three segments: rockets, Starlink, and AI.

When you split them apart, ‘reality hits you hard, bro’:

- Starlink (the Connectivity segment) made $11.4 billion in revenue and $4.42 billion in operating profit. It is the only profitable part of the company. Frankly, this business is baller!

- The rocket business lost money - a $657 million operating loss, mostly Starship development.

- The AI business lost $6.36 billion dollars in a single year.

Read that again. The satellite-internet business is profitable, and every dollar of that profit - and then some - is being poured into an AI division that’s losing money faster than the rest of the company earns it. Starlink is the engine. xAI is the (A)hole.

There’s a second tell. Starlink’s revenue per user dropped from 81 dollars to 66 dollars in a single quarter. Subscribers are up, price per subscriber is down. That’s a business buying growth by getting cheaper - ok, fine if you’re scaling toward dominance, less fine if the market’s pricing you as if the margins only go up.

Retail takes it up the clacker (yet again)

Here’s the line that should stop anyone thinking of buying SpaceX shares for their personal portfolio.

Musk holds about 42% of the equity, but after the IPO, he’ll control 82.4% of the voting power. For the sake of fu$k! The company runs a dual-class structure where his Class B shares carry ten votes each and the Class A shares sold to the public carry one. You get economic exposure. You get effectively no voice.

You don’t have to take my word that this matters. Major institutional pension powerhouses like CalPERS and the NYC Comptroller have been loudly fighting this exact kind of corporate governance breakdown across the market this year. When the institutions managing hundreds of billions in retirement capital put their objections to dual-class structures in writing, the retail buyer reading a hype thread on a Sunday night might want to ask why.

So this is the Musk structure: You fund it. He steers it. If you disagree with a decision, your $10K dropped on Class A shares is outvoted by a structure designed, on purpose, so that it doesn’t matter.

Listen, others have taken the piss in the manner in the past, and many will again. But why the fuck are we pretending this is a public company when one dude holds 82% of the voting rights?

There’s more than an element of Evil Wonka here…

The two rule changes that should bother you most

Nope, that’s not all folks! We got some rules rewritten to allow for further cluster-fuckery designed to benefit the current insiders and screw over those coming into the IPO. Two rules got rewritten for this IPO, and they’re built to work together.

1. The Index Fast-Track ("Lex SpaceX")

Normally, a newly listed company waits about three months - a “seasoning” period - before it can join the Nasdaq-100. That window gives the market time for natural price discovery. Effective May 1 this year, Nasdaq scrapped it for mega-caps. Any new listing ranking in the top 40 can now join the Nasdaq-100 after just 15 trading days, and the minimum float requirement was dropped entirely.

Because SpaceX is floating only a sliver of itself, Nasdaq applies a weighting multiplier - up to three times the float - treating it as far bigger than its tradable shares justify. Index trackers have to buy accordingly. Estimates suggest $22 to $27 billion of automatic, price-blind buying will flood in from Nasdaq-100 trackers in the first weeks.

The Adult in the Room: S&P Global held the line. On June 4, they refused to loosen their rules, meaning SpaceX can’t enter the S&P 500 until at least mid-2027. FTSE Russell and Nasdaq, however, completely folded.

2. Rule change two: the insider unlock.

A standard IPO locks insiders out of selling for 180 days to stabilise the stock. SpaceX negotiated a front-loaded schedule starting early, unlocking tranches at 70, 90, 105, 120, and 135 days, with an extra slice freed up if the stock trades 30% above IPO price.

Connect the dots: CNBC pointed out that the early unlock schedule perfectly matches the fast-entry rule. Index inclusion triggers a massive wave of forced, price-blind institutional buying around day 15. The early-unlock schedule allows insiders to sell their shares directly into that engineered demand wave of your superannuation fund!

The passive money - your super, the index trackers, every fund that has to hold what the benchmark holds - becomes the loser on that trade.

None of this is illegal. None of it is hidden; it’s in the filing and the index methodology. It’s just a very good deal for the people who already hold the shares, paid for by the people who never chose to.

There are always two sides to the trade, people!

OpenAI and Anthropic: growth that’s real, maths that might not quite be…

The AI pair are a different flavour of the same question.

OpenAI’s revenue is genuinely staggering - an annualised run-rate around $25 billion by March, from basically nothing three years ago. But it’s projected to lose about $14 billion at the operating line in 2026, and doesn’t expect to be cash-flow positive until 2030. That right there is a pickle, my friend! You might be able to sustain that if you don’t have competition, but if you do…

One analysis pegged it at losing a dollar twenty-two for every dollar of revenue earned in the first quarter. Sitting underneath that is a compute commitment of roughly $600 billion over five years, with some deals stretching toward $1.4 trillion over eight. That 1.4 trillion figure is the one doing the rounds in the headlines - it’s not the valuation, it’s the bill.

At its target valuation, OpenAI would be priced at something like 65 times its 2025 revenue. For comparison, most mature software companies trade at a small fraction of that.

Anthropic’s run-rate reportedly hit $47 billion by May, up from $10 billion a year earlier. The growth is real. But the filing is confidential, which means there is no audited profit-or-loss line in public yet. So when you see someone confidently quoting Anthropic’s “profitability,” ask them where the number came from. It isn’t in a public document.

This is the actual Perception Check

I’m not here to tell you AI is a bubble or that space is a scam. The businesses are real. Starlink is a genuine monopoly-in-the-making. The AI revenue curves are unlike anything in tech history.

The check is this: size is being used as a substitute for thinking.

“Largest IPO in history” is doing a lot of work in these stories. It’s meant to feel like a reason to invest. It isn’t. Largest is a measure of how much money is involved, not whether the price makes sense. A trillion-dollar valuation on a company losing billions a year isn’t validated by the trillion - the trillion is the thing you’re supposed to be checking. And this is before we take in that one dude controls 82% of the voting rights. That is just insane!

And where is this new capital coming from? If four trillion in value gets sucked toward three names, doesn’t it have to leave somewhere else? Markets aren’t a fixed pie in the short run; new money enters, leverage expands. But raises this large absolutely create rotation pressure, and there’s live talk of money already moving out of semiconductors to fund the trade. These bets are so large, and the forced index-buying so mechanical, that they concentrate risk in a way that touches portfolios that never opted in. Including - if any of your assets touch the capital markets - yours.

Find out what you already own. Log into your super, find the investment option you’re in, and look at the top holdings of any “international shares” or “indexed global” portion. You’re checking for two things: how exposed you already are to the handful of mega-cap tech names driving this, and what gets added when these three list. You’re not deciding to sell or hold. You’re just refusing to be a shareholder in something this big without knowing it. The number of people who can name their own super’s top ten holdings is roughly the number of people who won’t be surprised in 2027.

Annnnnd, GO!

Ben

#BeAVillager

P.S. The detail that’s arguably corrupt: the seasoning period Nasdaq waived - the three-month wait before index inclusion - exists precisely so the market can find a real price before trillions in passive money is forced to buy. Waiving it doesn’t just speed things up. It removes the price-discovery window and replaces it with forced demand, right around the time insiders are cleared to sell. Musk didn't break the rules. According to Reuters, SpaceX signalled fast inclusion was a condition of where it listed - and the rules moved. You're allowed to draw your own conclusion about what that is.

This is commentary, not financial advice. I’m a founder, not a licensed adviser - every figure here is from public filings and reporting, linked in the references, and none of it is a recommendation to buy, sell or hold anything. Do your own work, or talk to someone licensed to give you advice.

References

- SpaceX S-1 (SEC, filed 20 May 2026; S-1/A 3 June 2026): 2025 revenue $18,674m, operating loss $2,589m, Adjusted EBITDA $6,584m

- Yahoo Finance / Via Satellite / The Motley Fool / Inc. (May 2026): segment breakdown - Starlink $11.4bn revenue and $4.42bn operating profit; AI segment $6.36bn 2025 loss; 2024 net profit $791m; Starlink ARPU $81 to $66

- SpaceX S-1 (SEC, filed 20 May 2026; S-1/A 3 June 2026): Musk ~42% equity, 82.4% voting power post-IPO; Class B 10 votes vs Class A 1 vote

- AIxploria / Roborhythms / CMC Markets (May–June 2026): OpenAI ~$25bn annualised run-rate, ~$14bn projected 2026 operating loss, cash-flow positive target 2030, ~$600bn–$1.4tn compute commitments, ~65x revenue multiple

- Futurum / CNBC / Fortune (June 2026): Anthropic $65bn Series H at $965bn valuation, ~$47bn run-rate, confidential S-1 filed 1 June, October 2026 target

- Fortune (June 2026): “The S&P 500 will initially exclude SpaceX but Elon Musk is coming for your retirement savings anyway” - index-inclusion / forced-buying mechanism

- SpotGamma / heise / Reuters (Apr–June 2026): Nasdaq-100 fast-entry rule effective 1 May 2026 - 15 trading days vs 3-month seasoning, float minimum eliminated, low-float weighting multiplier up to 3x; est. $22–27bn forced Nasdaq-100/Russell buying; “Lex SpaceX”

- CNBC (5 June 2026): S&P Global declined to shorten its 12-month seasoning or waive profitability/float tests; SpaceX ineligible for S&P 500 until ~mid-2027; FTSE Russell granted fast entry

- CNBC (21 May 2026): SpaceX insider lock-up - front-loaded unlock schedule (70/90/105/120/135 days, extra tranche if 30% above IPO price) designed to align with fast-entry forced buying

- Bloomberg Intelligence via Yahoo Finance (June 2026): estimated forced passive buying from fast S&P inclusion - ~$14bn SpaceX, >$8bn OpenAI, ~$4.6bn Anthropic (now off the table after S&P decision)